X

The institutional investors who invest in the Indian Debt Market are:

Retail investors are allowed to invest in select issuances though their participation is in evolving phase.

Money Market and Government Securities markets are regulated by the Reserve Bank of India (RBI). Whereas, other fixed income instruments (PSU bonds, Non-Convertible Debentures, etc.) are regulated by both, RBI and SEBI (Securities and Exchange Board of India).

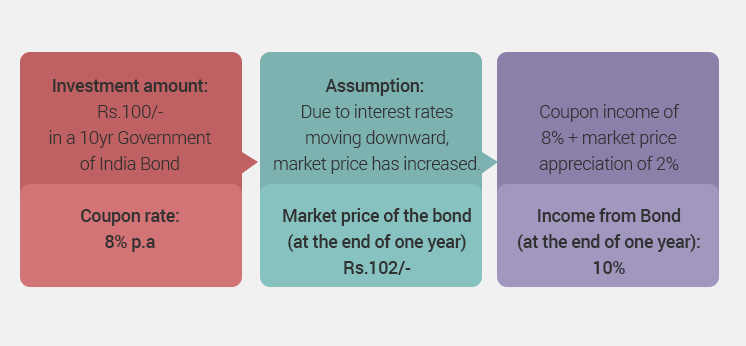

The Yield to maturity (YTM) is the internal rate of return earned by an investor assuming that the bond will be held until maturity, and that all coupon and principal payments will be made on schedule. It basically measures the total income earned by the investor over the entire life of the security.

This total income consists of three components:

OMOs is a tool used by the Reserve Bank of India to adjust the rupee liquidity conditions in the market. When the RBI feels there is excess liquidity in the market, it resorts to sale of securities thereby sucking out the rupee liquidity. Similarly, when the liquidity conditions are tight, the RBI will buy securities from the market, thereby releasing liquidity into the market.

Various credit rating agencies evaluate the credit worthiness of entities issuing debt instruments. This rating helps investors to make an informed decision before investing in any debt instrument.

The rating is given as an alphanumeric code that represents a graded structure or creditworthiness. Private independent rating services such as CRISIL, ICRA, CARE, and FITCH provide these evaluations.

Few ratings and their implications:

| Rating | Rank | Implication |

|---|---|---|

| AAA Rating | Highest credit rating | Implies a high credit quality and a small chance of default |

| D (for default) | Lowest credit rating | Implies a very risky investment |

Few of the common fixed income instruments are:

A fixed income security is issued by Government, corporates or other entities. The security represents a loan that is offered by an investor to an entity. As the name suggests, a fixed income security offers fixed periodic interest (known as coupon payment) to the investor.

There is an active secondary market (for purchasing securities from other investors) in G-secs. The securities can be bought / sold by investors in the secondary market either:

Few of the factors which govern interest rates are:

LAF is offered by RBI to scheduled commercial banks and primary dealers for liquidity management on a day to day basis. Under LAF, these banks and dealers can approach RBI:

This facility is available on an overnight basis, against the collateral of Government securities including State Government securities.

The accrued interest on a bond is the amount of interest accumulated on a bond since the last coupon payment (interest payment). The interest has been earned, but because coupons are paid only on coupon dates, the investor has not gained the money yet. In India, day count convention for G-secs is 30/360.

A yield curve is a line that plots the interest rates on Y-axis and maturity dates on X-axis. The shape of the yield curve gives an idea of future interest rate change and economic activity.

| Type of Yield Curve | Feature | Implication |

|---|---|---|

| Normal | Longer maturity bonds have a higher yield compared to shorter-term bonds | Risks associated with time |

| Inverted | Shorter-term yields are higher than the longer-term yields | A sign of upcoming recession |

| Flat (or humped) | Shorter- and longer-term yields are very close to each other | A predictor of an economic transition |

Fixed income investments are a secure and low-risk way to generate a steady flow of income. Investment in fixed income securities should be an important part of a well-diversified portfolio.

If interest rates or market yields decline, the price of a bond rises. Conversely, if interest rates or market yields rise, the price of the bond falls. In other words, the yield of a bond is inversely related to its price.

Duration is the payback period of a bond to break even, i.e., the time taken for a bond to repay its own purchase price. Duration is expressed in number of years. Duration is useful primarily as a measure of the sensitivity of a bond's market price to interest rate (i.e., yield) movements. It is approximately equal to the percentage change in price for a given change in yield.

DigiLocker, the National Digital Locker System launched by the Government of India can be accessed using the below URLs:

Here are the steps (if you have not linked Aadhaar to your DigiLocker account):

Here are the steps to get e-Policy in DigiLocker (if you have linked Aadhaar to your DigiLocker account):

Please visit https://digilocker.gov.in/faq.html