X

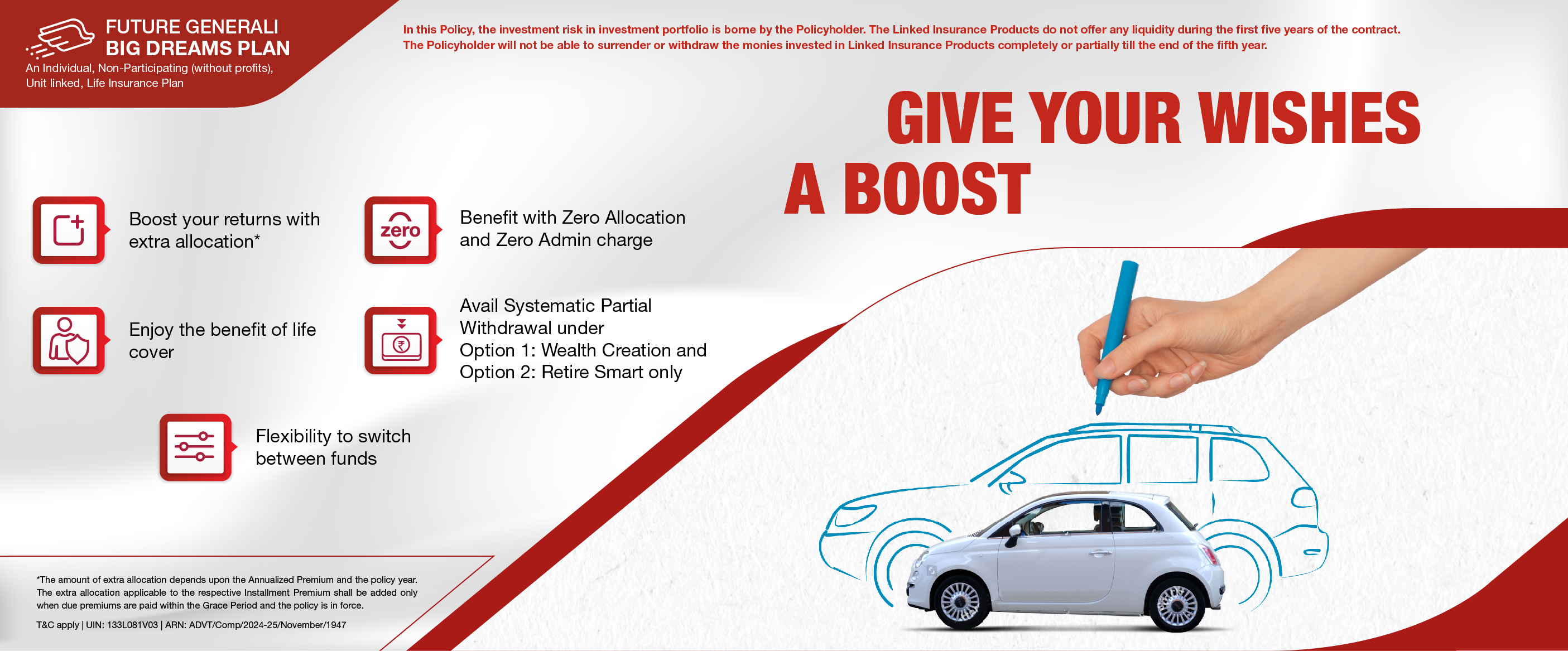

We all want a little extra something in life. Same is true for our investments as well, so we have created a Unit Linked Insurance Plan just for that. With us, you can now dream much more.

Presenting the Future Generali Big Dreams Plan, a comprehensive Unit Linked Insurance Plan, that lets you create wealth while enjoying the benefits of an insurance plan at the same time.

So go on and secure your long-term future and dreams!

Boost your returns with extra allocation, from 1% to 7% on your each instalment premium if the due premium is paid within the Grace Period. This ensures you reach your financial goals faster.

Benefit with Zero Allocation and Zero Admin charge and watch your wealth grow faster.

Enjoy the benefit of life cover and secure your family’s future against the uncertainties of life.

Fulfil your life’s goals by choosing from 3 available options – Wealth Creation, Retire Smart and Dream Protect.

Avail Systematic Partial Withdrawal (under Option 1: Wealth Creation and Option 2: Retire Smart only) and receive money in your account monthly to help you meet specific financial requirements.

Get the flexibility to change your funds and always be in complete control of your wealth.

Avail tax benefits under Section 80C and Sec 10(10D) of the Income Tax Act of 1961. These benefits are subject to change as per the prevailing tax laws.

Choice of two optional rider to match your specific needs.

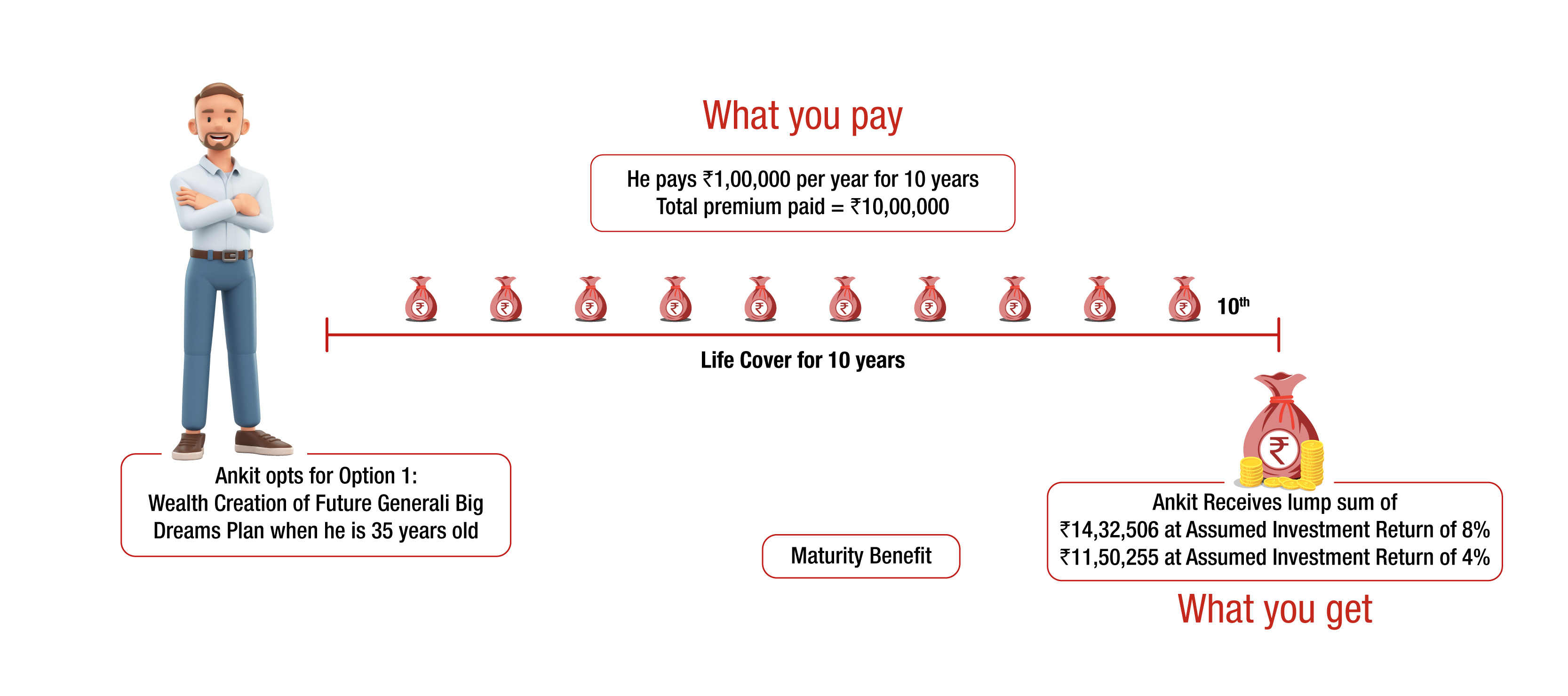

Ankit is 35 years old and has chosen to invest in Option 1: Wealth Creation of the Future Generali Big Dreams Plan, with a Policy Term of 10 years, an annual premium of Rs. 1,00,000 for 10 years,His Death Benefit Multiple is 10 times and a Sum Assured (cover amount) of Rs. 10,00,000.

Note: For the purpose of illustration, we have assumed 8% p.a and 4% p.a as the higher and lower values of investment returns. These rates are not guaranteed, and they are not the upper or lower limits of returns of the Funds selected in your policy, as the performance of funds depends on several factors including future investment performance. These rates in no way signify our expectations of future returns and the actual returns may be higher or lower.

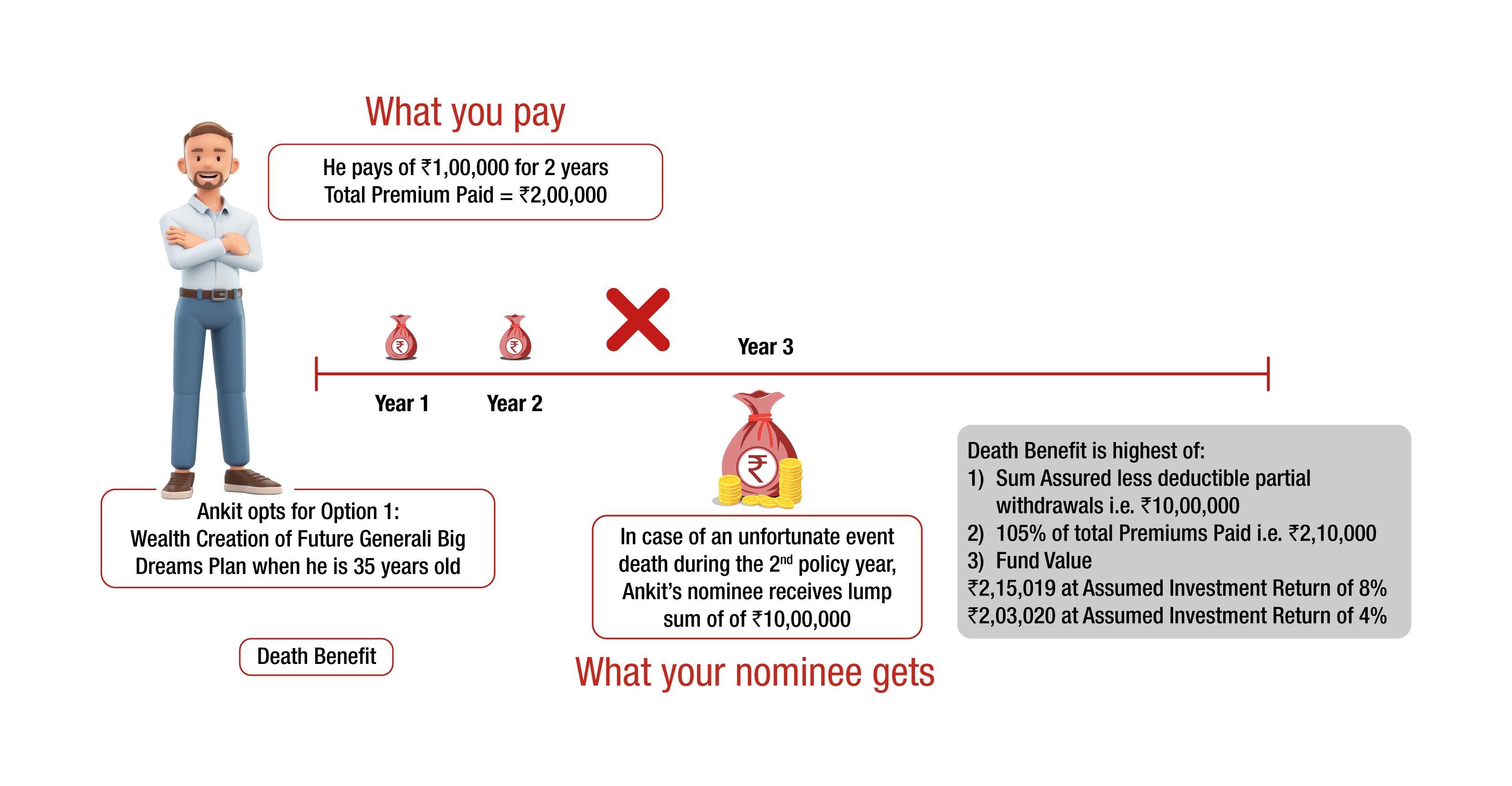

In case of your unfortunate demise, the Death Benefit in this plan secures your family’s financial well-being and future. The Death Benefit varies as per the plan option you choose:

The Death Benefit payable to the nominee shall be the higher of:

The Policy will terminate on the payment of Death Benefit.

To clearly understand how the death benefit works, let us refer to Ankit’s story.

Like we discussed, Ankit is 35 years old, and has invested in Option 1:Wealth Creation of the Future Generali Big Dreams Plan, with a Policy Term of 10 years and Death Benefit Multiple is 10 times, In case of Ankit’s unfortunate death after having paid just 2 premiums, the following illustration shows what his nominee will get:

Note: For the purpose of illustration, we have assumed 8% p.a and 4% p.a as the higher and lower values of investment returns. These rates are not guaranteed, and they are not the upper or lower limits of returns of the Funds selected in your policy, as the performance of funds depends on several factors including future investment performance. These rates in no way signify our expectations of future returns and the actual returns may be higher or lower.

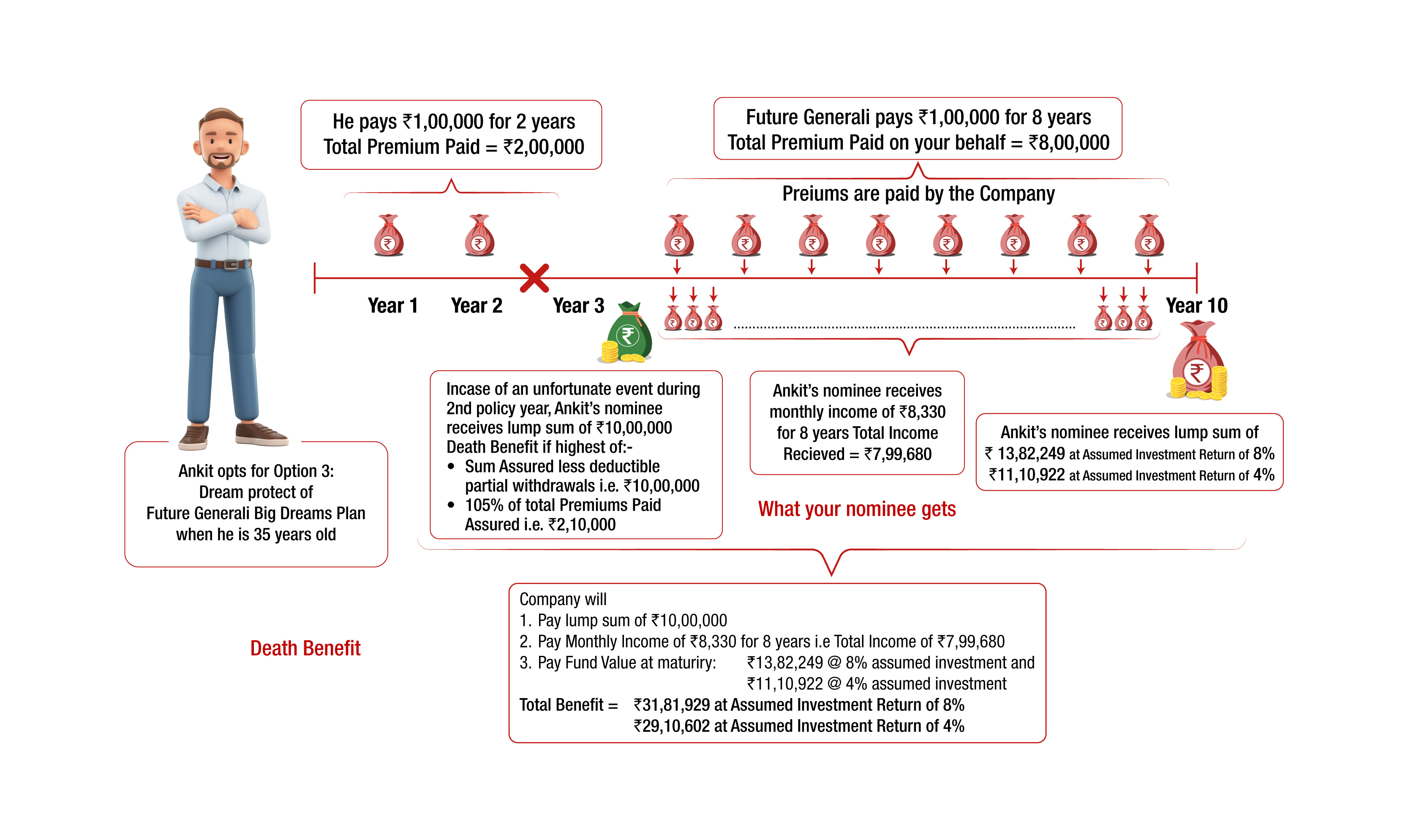

In addition:

The Policy will terminate on the complete payment of Maturity Benefit at the end of the Policy Term.

To clearly understand how death benefit works in this case, let us look at Ankit’s story had he chosen Option 3:Dream Protect option, with a Policy Term of 10 years and Death Benefit Multiple is 10 times, The following illustration shows what his nominee will get in case of Ankit’s unfortunate death, after paying just 2 premiums:

Note :For Deductible Partial Withdrawals applicable under Death Benefit for all plan options: Deductible partial withdrawals are partial withdrawals made in the 2 years prior to the date of death of the Life Assured.

For the purpose of illustration, we have assumed 8% p.a and 4% p.a as the higher and lower values of investment returns. These rates are not guaranteed, and they are not the upper or lower limits of returns of the Funds selected in your policy, as the performance of funds depends on several factors including future investment performance. These rates in no way signify our expectations of future returns and the actual returns may be higher or lower.

Wealth Creation- If your need is to save for a specific milestone, this option is for you. For e.g. this option is perfect if you are looking to buy a house, start your own business, pursue your education or achieve any other important life goal.

After the completion of your premium payment term, you can utilize the accumulated corpus to get monthly income using our systematic partial withdrawal feature.

Retire Smart- Say goodbye to your retirement worries with this option. Build a retirement corpus and get monthly income* any time after you have completed your premium payment term using our systematicpartial withdrawal feature.

*Enjoy tax benefit as per prevailing tax laws.

Dream Protect- Choose this option to secure the dreams of your loved ones even when you are not around. Build a corpus fund for your child’s higher education, or forthe financial security of your spouse/parents. The option will continue even in the case of your unfortunate demise,and your nominee(s) will get the following benefits:

Now that you have chosen your option, you have a few more things to decide basis your financial goals:

After everything else has been decided, you need to choose your fund allocation strategy. This plan gives you two options.

Then you may choose from the optional riders provided to get additional benefits to enhance coverage and tailor the policy to your specific needs at nominal cost. This plan gives you two options:

Finally, fill in the application form, pay your premiums and submit all the necessary documents.

|

Min Entry Age 0 |

Max Entry Age 65 |

|

Min Maturity Age 18 |

Max Maturity Age 85 |

| Minimum Premium( in Rs) | ||

| Policy Term( in Years) | 5 to 9 | 10 & above |

|---|---|---|

| Single | 1,00,000 | 1,00,000 |

| Annual | 60,000 | 18,000 |

| Semi - Annual | 30,000 | 9,000 |

| Quarterly | 15,000 | 4500 |

| Monthly | 5,000 | 1,500 |

| Maximum Premium (in Rs.): No Limit (Subject to Board Approved Underwriting Policy) | ||

| Regular Pay | 0 to 55 years = 10 times * Annualized Premium, 56 to 65 years = 5 & 7 times * Annualized Premium |

| Limited Pay | 0 to 55 years = 10 times * Annualized Premium, 56 to 65 years = 5 & 7 times * Annualized Premium |

| Single Pay | 0 to 55 years = 1.25 times * Single Premium, 56 to 65 years = 1.10 times * Single Premium. |

|

5 to 20 years |

|

|

Premium Payment Term |

|

| Regular Pay | Equal To Policy Term |

| Limited Pay | 5 to 19 years |

| Single Pay | One Time Premium Payment |

|

Single Pay, Yearly, Half Yearly, Quarterly, Monthly |

|

Min Entry Age 18 |

Max Entry Age 65 |

|

Min Maturity Age 100 |

Max Maturity Age 100 |

| Minimum Premium( in Rs) | ||

| Policy Term( in Years) | 5 to 9 | 10 & above |

|---|---|---|

| Single | 1,00,000 | 1,00,000 |

| Annual | 60,000 | 18,000 |

| Semi - Annual | 30,000 | 9,000 |

| Monthly | 5,000 | 1,500 |

| Quarterly | 15,000 | 4500 |

| Maximum Premium (in Rs.): No Limit (Subject to Board Approved Underwriting Policy) | ||

| Regular Pay | NA |

| Limited Pay | 18 to 55 years = 10 times * Annualized Premium, 56 to 65 years = 5 & 7 times * Annualized Premium |

| Single Pay | NA |

|

100 – Age at entry |

|

|

Premium Payment Term |

|

| Regular Pay | NA |

| Limited Pay | 10 years to 30 years |

| Single Pay | NA |

|

Yearly, Half Yearly, Quarterly, Monthly |

|

Min Entry Age 18 |

Max Entry Age 45 |

|

Min Maturity Age 23 |

Max Maturity Age 65 |

| Minimum Premium( in Rs) | ||

| Policy Term( in Years) | 35 to 82 years | 10 & above |

|---|---|---|

| Single | 1,00,000 | 1,00,000 |

| Annual | 60,000 | 18,000 |

| Semi - Annual | 30,000 | 9,000 |

| Quarterly | 15,000 | 4500 |

| Monthly | 5,000 | 1,500 |

| Maximum Premium (in Rs.): No Limit (Subject to Board Approved Underwriting Policy) | ||

| Regular Pay | 18-45 years = 10 times * Annualized Premium |

| Limited Pay | NA |

| Single Pay | NA |

|

5 to 20 years |

|

|

Premium Payment Term |

|

| Regular Pay | Equal to Policy Term |

| Limited Pay | NA |

| Single Pay | NA |

|

Yearly, Half Yearly, Quarterly, Monthly |

Premium Allocation Charge: Nil

Policy Administration Charge: Nil

Discontinuance Charge

In case of discontinuance of the policy during the first 4 policy years, the following charges will apply.

| Discontinuance during the policy year | Discontinuance Charge (AP <= Rs 50, 000) | Discontinuance Charge (AP >Rs 50, 000) |

|---|---|---|

| 1 | Lower of 20% x (AP or FV), subject to a maximum of Rs. 3,000 | Lower of 6% x (AP or FV), subject to a maximum of Rs. 6,000 |

| 2 | Lower of 15% x (AP or FV), subject to a maximum of Rs. 2,000 | Lower of 4% x (AP or FV), subject to a maximum of Rs. 5,000 |

| 3 | Lower of 10% x (AP or FV), subject to a maximum of Rs. 1,500 | Lower of 3% x (AP or FV), subject to a maximum of Rs. 4,000 |

| 4 | Lower of 5% x (AP or FV), subject to a maximum of Rs. 1,000 | Lower of 2% x (AP or FV), subject to a maximum of Rs. 2,000 |

| 5 and onwards | NIL | Nil |

where,

AP = Annualised Premium under the policy

FV = Fund Value on the date of discontinuance

| For Single Pay Policy | ||

|---|---|---|

| Discontinuance during the policy year | Discontinuance Charge | |

| (SP<= Rs. 3,00,000) | (SP> Rs. 3,00,000) | |

| 1 | Lower of 2% x (SP or FV), subject to a maximum of Rs 3,000 | Lower of 1% *(SP or FV) subject to a maximum of Rs. 6,000 |

| 2 | Lower of 1.5% x (SP or FV), subject to a maximum of Rs 2,000 | Lower of 0.70% *(SP or FV) subject to a maximum of Rs.5,000 |

| 3 | Lower of 1% x (SP or FV), subject to a maximum of Rs 1,500 | Lower of 0.50% *(SP or FV) subject to a maximum of Rs.4,000 |

| 4 | Lower of 0.5% x (SP or FV), subject to a maximum of Rs 1,000 | Lower of 0.35% *(SP or FV) subject to a maximum of Rs.2,000 |

| 5 and onwards | NIL | NIL |

where,

SP = Single Premium under the policy

FV = Fund Value on the date of discontinuance

Fund Management Charge

| Fund management charge (% p.a.) | |

|---|---|

| Future Income Fund (SFIN: ULIF002180708FUTUINCOME133) | 1.35% |

| Future Balance Fund (SFIN:ULIF003180708FUTBALANCE133) | 1.35% |

| Future Maximize Fund (SFIN:ULIF004180708FUMAXIMIZE133) | 1.35% |

| Future Apex fund (SFIN: ULIF010231209FUTUREAPEX133) | 1.35% |

| Future Opportunity Fund (SFIN: ULIF012090910FUTOPPORTU133) | 1.35% |

| Future Midcap Fund (SFIN:ULIF014010518FUTMIDCAP133) | 1.35% |

| Future Income Spark Fund (SFIN: ULIF022211124INCOMESPAR133) | 1.25% |

| Future Income Plus Fund (SFIN: ULIF023211124INCOMEPLUS133) | 1.35% |

| Future Multicap Equity Fund (SFIN: ULIF024211124MULTICAPEQ133) | 1.35% |

Fund Management Charges are deducted on a daily basis at 1/365th of the annual charge in determining the unit price.

Switching Charge: Nil

Partial Withdrawal Charge: Nil

Mortality Charge

For Option 1: Wealth Creation and Option 2: Retire Smart

Higher of (Sum assured less Deductible Partial Withdrawal or 105% of total premiums paid less Deductible Partial Withdrawal) less Fund Value under the policy.

For Option 3: Dream Protect

Higher of (Sum assured less Deductible Partial Withdrawal or 105% of total premiums paid less Deductible Partial Withdrawal) plus Discounted Value of future premium to be paid by the company and Discounted Value of Monthly Income Benefit payable, both at a discount rate of 6.85% p.a. compounded annually.

Miscellaneous charges: Nil

Revision of charges:

After obtaining appropriate approval, the Company reserves the right to revise the following charges:

However, premium allocation charge, discontinuance charge and mortality charges are guaranteed.

Timely payment of all your due premiums within grace period ensures that an extra allocation is added to the fund along with your Instalment Premium.

Extra Allocation amount = Extra Allocation Rate applicable for the policy year X Instalment Premium paid in that year within the grace period.

| Extra Allocation Rate applicable on Each installment Premium | ||

|---|---|---|

| Policy Year | Annualised Premium less Than Rs. 60,000 | Annualised Premium Rs. 60,000 and above |

| 1 to 5 | NIL | 1.0% |

| 6 to 8 | NIL | 3.0% |

| 9 to 10 | NIL | 4.0% |

| 11 to 15 | NIL | 5.0% |

| 16 to 30 | NIL | 7.0% |

Note: The extra allocation applicable to the respective Instalment Premium shall be added only when due premiums are paid within the Grace Period and the policy is in force.

| Policy Year | Extra Allocation Rate applicable on Single Premium |

|---|---|

| 1 | 1% |

| 2 to 20 | NIL |

At any time, the policyholder may instruct us in writing to switch some or all the units from one unit linked fund to another, except switches to and from the Discontinuance Fund. The company will give effect to this switch by cancelling units in the old fund(s) and allocating units to the new fund(s) at the applicable unit price. The amount to be switched should be at least Rs. 5,000. The switch request shall be processed as per the IRDAI guidelines.

At any time after completion of one year, the policyholder may instruct us in writing,before the next premium due date,to redirect all future premiums in an alternative proportion to the various unit funds available. Redirection will not affect the premiums paid prior to the request. A maximum of two premium redirections are allowed in a policy year.

At any time after the completion of the lock-in period of 5 years from the policy commencement date, the policyholder may instruct us in writing to withdraw fund value partially from the policy. Unlimited free partial withdrawals that can be done in this plan. The minimum fund value after the partial withdrawal shall be at least 105% of the Total Premiums Paid (including top-up premiums paid, if any) during the premium payment term and one annualized premium after the premium payment term for Regular and Limited pay policies and at least Rs. 10,000 for Single pay policies.

Systematic Transfer Option (STO) is a feature which allows auto switching of units from one segregated fund to another segregated fund. You have the option to weekly transfer the Fund Value available under one specific Fund to another fund by making a written request to the Company. Once this feature is used, the Fund Value available under one specific fund will be transferred to another fund on a weekly basis for 48 weeks. The policyholder can submit STO request anytime during the policy term. The policyholder cannot make another STO request until the current STO instruction has been completed or has been cancelled.

The fund from which the units will be transferred is called the ‘Selected Fund’ and the fund to which the units will be deposited is called the ‘Target Fund’. At any point in time, a STO request is only applicable between anyone Selected Fund and anyone Target Fund. The remaining 7 funds will not be affected or participate in the STO.

Once a STO request is placed, units from the Selected Fund will be transferred to the Target Fund through 48 automatic switches on the 7th, 14th, 21st and 28th of each calendar month for a 12-month period. Under every automated switch in a given STO, 1/Xth of units from the Selected Fund will be transferred to theTarget Fund, Where X = no of automatic switches which are left to be done in the given STO request i.e. X will be 48 for the first automated switch, it will be 47 for the second automated switch and it will be 1 for the 48th automated switch.

Premiums by Policyholder can come in any of the 9 segregated funds. Future premium redirection can be done in any of the 9 segregated funds.

However, during the period in which STO is invoked, no switching can take place in any of the 9 segregated funds.

The policyholder has the option to stop the STO by providing a written request to the Company. Once the STO is stopped, the policyholder can switch units between segregated funds as needed.

A policyholder can make further STO requests after the completion of a previous STO request. STO will apply to both future premiums as well as existing premiums in the Selected Fund. The NAV applicable for STO will be the NAV of the Selected Fund and target fund on the day when the STO takes effect.

STO will not be activated when Auto Invest Rule is active

For Option 3: Dream Protect, STO request will not be allowed after the death of the Life Assured.

STO will stop if:

There are no charges for STO.

This feature allows the policyholder to withdraw a monthly amount from the policy during the policy term. This feature is only available under Option 1: Wealth Creation and Option 2: Retire Smart. At any time during the policy term after the end of the lock-in period, the policyholder may request us to make systematic partial withdrawals from the fund under the policy. The policyholder shall be required to specify the withdrawal start date, amount of withdrawal and the number of withdrawals to be done in the request. The monthly amount withdrawn from the fund shall be paid at the end of each calendar month following the withdrawal start date.

The conditions for systematic partial withdrawal are:

Systematic Partial Withdrawal will stop if any of the following is triggered:

No charges shall be deducted for Systematic Partial Withdrawal.

The plan offers two fund allocation strategies which can be chosen at the start of the policy or at any time during the policy term. The policyholder can request to change the fund allocation strategy anytime during the policy term.

| Funds | Fund Allocation and Premium Allocation Percentage |

|---|---|

| Future Apex Fund or Future Midcap Fund as chosen by the policyholder | [100- Current Age of the Policyholder (Age as on his/her last birthday)] % |

| Future Income Fund | [Current Age of the Policyholder (Age as on his/her last birthday)] % |

| Outstanding years to maturity of the policy (as on last policy anniversary) | Fund Allocation and Premium Allocation Percentage to Future Apex Fund or Future Midcap Fund as chosen by the policyholder | Fund Allocation and Premium Allocation Percentage to Future Income Fund |

|---|---|---|

| 16 and more | 100% | 0% |

| 11 to 15 | 80% | 20% |

| 9 to 10 | 60% | 40% |

| 6 to 8 | 40% | 60% |

| 1 to 5 | 20% | 80% |

You may return this Policy within 30 days of receipt of the Policy Document (whether received electronically or otherwise), if You disagree with any of the terms and conditions by giving Us a request for cancellation of this Policy which states the reasons for Your objections.

On cancellation of the Policy after such request , You shall receive the Fund Value as on the date of cancellation of the Policy plus non-allocated Premium, if any plus charges levied by cancellation of Units minus (Stamp duty + medical expenses, if any, + proportionate risk premium for the period on cover) minus Extra Allocation added to the Policy.

If the Policy is opted through Insurance Repository (IR), the computation of the said Free Look Period will be as stated below:

Grace period means the time granted by the insurer from the due date of payment of premium, without any penalty or late fee, during which time the policy is considered to be in-force with the risk cover without any interruption, as per the terms & conditions of the policy. The grace period for payment of the premium for all types of life insurance policies shall be fifteen days, where the policyholder pays the premium on a monthly basis and 30 days in all other cases.Grace Period is not applicable under the single pay policy.

For further information on these riders including risk factors, exclusions, terms and conditions etc., please refer the rider/s brochures available on the website at www.futuregenerali.in or contact us at Email – care@futuregenerali.in , Customer Care Number – 1800-102-2355.

No loan is allowed under this product.

In case of death of Life Assured due to suicide within 12 months from the date of commencement of the policy or from the date of revival of the policy, as applicable, the nominee or the beneficiary of the policyholder shall be entitled to the fund value, as available on the date of intimation of death.

Further, any charges other than Fund Management Charges (FMC) and Guarantee Charges recovered subsequent to the date of death shall be added back to the fund value as on the date of intimation of death.

We will provide a resolution at the earliest. For further details please access the link: https://life.futuregenerali.in/customer-service/grievance-redressal-procedure

For customers looking for a tax saving systematic investment solution which helps to get market linked returns along with benefits of insurance

Future Generali Big Dream Plan (UIN: 133L081V03)

This Product is not available for online sale.Life Coverage is included in this Product. For detailed information on this plan including risk factors, exclusions, terms and conditions etc., please refer to the product brochure and consult your advisor, or, visit our website before concluding a sale. Tax benefits are as per the Income Tax Act 1961 and are subject to any amendment made thereto from time to time. If you have any request, grievance, complaint or feedback, you may reach out to us at care@futuregenerali.in For further details please access the link: https://life.futuregenerali.in/customer-service/grievance-redressal-procedure.

Future Generali Big Dreams Plan is an Individual, Non-Participating (without profits), Unit Linked, Life insurance plan.

No, the Plan option needs to be chosen at the outset of the Policy.

Once chosen, the Policyholder shall not be allowed to change the option during the policy term

Individuals, Residents and Non Resident Indians, PIO & Foreigners (subject to Underwriting) can be covered under Future Generali Big Dreams Plan

Self & Partner Branches

Individual claims settlement ratio for FY 2023-2024

Lives covered since inception

Worth of Asset Under Management

Data as on 31st March 2025