X

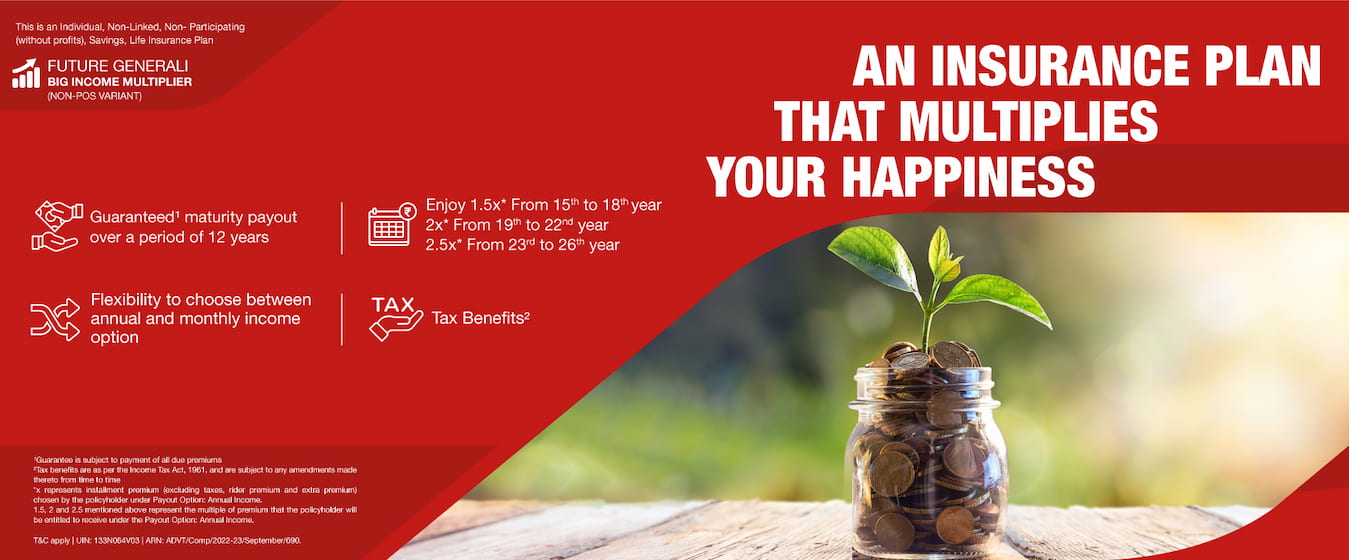

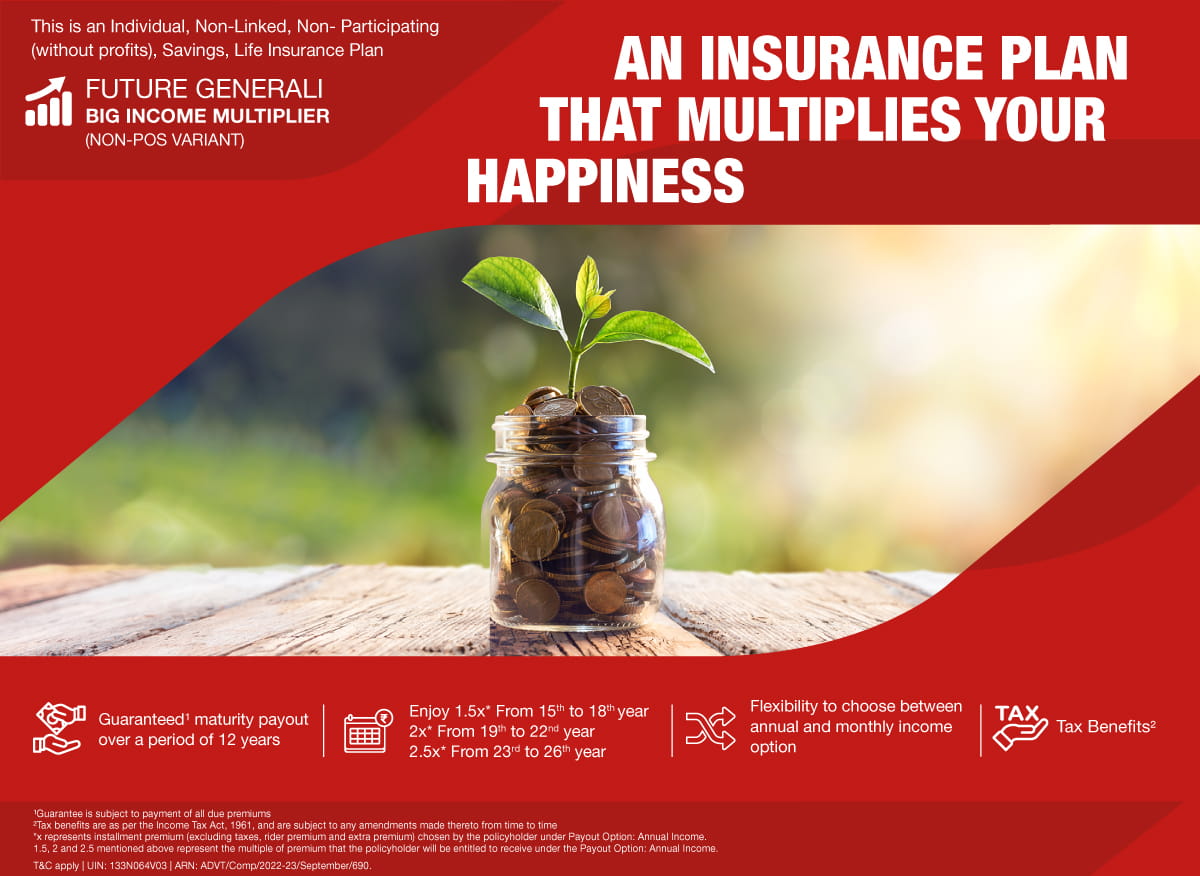

As Indian’s we all excel at making the most of our resources and this is especially true when it comes to our hard earned money. Wouldn’t it excite you to know that there is a financial solution which does just that and helps you generate twice the value for every rupee you save.

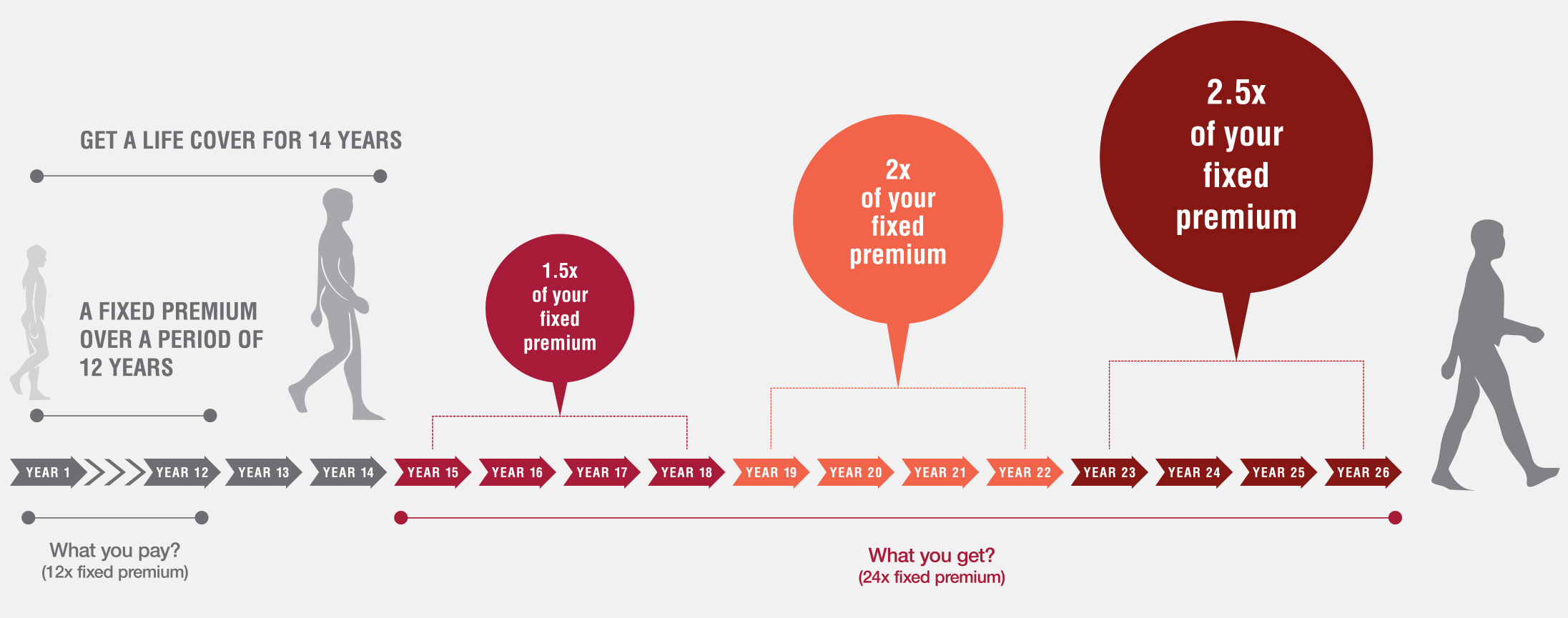

Presenting Future Generali Big Income Multiplier, a life insurance plan which guarantees Double Returns over the payout period. Here’s how the plan works in a nutshell

Choose a payout option

i) Annual Income Payout Option or

ii) Monthly Income Payout Option to receive income as per your desired frequency.

Choose the amount of premium you would like to pay under this life insurance plan

Pay the desired premium amount for 12 years. The premium payment frequency will be annual for Annual Income Payout Option and monthly for Monthly Income Payout Option.

Receive guaranteed income for 12 years after the end of policy term as per your life insurance plan option.

| Parameter | Criterion |

|---|---|

| Entry Age | 4 years to 50 years (Age means your age as on your last birthday) |

| Maturity Age | 18 years to 64 years |

| Policy Term | Fixed Policy Term of 14 years |

| Premium Payment Term | Fixed Premium Payment Term of 12 years |

| Life Insurance Plan Options | Payout Option:- Annual Income Payout Option:- Monthly Income |

| Premium Payment Frequency | Annual Income Payout Option :- Annual mode Monthly Income Payout Option :- Monthly mode |

| Minimum Instalment Premium | Annual Income Payout Option :- Rs. 18,000 Monthly Income Payout Option :- Rs. 1,500 |

| Maturity Sum Assured | For Annual Income Payout Option:- 15.8782 X Annual Premium For Monthly Income Payout Option:- 184.4113 X Monthly Premium |

| Payout Term | Payout term is 12 years after the end of policy term |

Note -

For a minor Life Assured, the risk will commence immediately on the policy commencement date.

Maturity Benefit:

If you have paid all your premiums, you will receive the following benefits after your policy matures.

| Your Benefits | Payout Option: Annual Income | Payout Option: Monthly Income |

|---|---|---|

Maturity Benefit |

Provided the premium payment frequency chosen is annual,

|

Provided the premium payment frequency chosen is monthly,

|

| Total Benefit Payable | 2 times of Total Premium paid under the policy | 2 times of Total Premium paid under the policy |

You may take your Maturity Benefit as lump sum at the Maturity Date by selecting the said option at the inception of the policy. The lump sum Maturity Benefit is equal to the Maturity Sum Assured i.e. lump sum maturity benefit is equal to 15.8782 times annual premium in case of Annual income pay out option and is equal to 184.4113 times monthly premium in case of monthly income pay out option.

Note: The Annual Premium and Monthly Premium mentioned in the table above is excluding taxes, rider premiums, extra premium and cess, if any.

‘Payout period’ means the period over which the payouts under Maturity Benefit are payable.

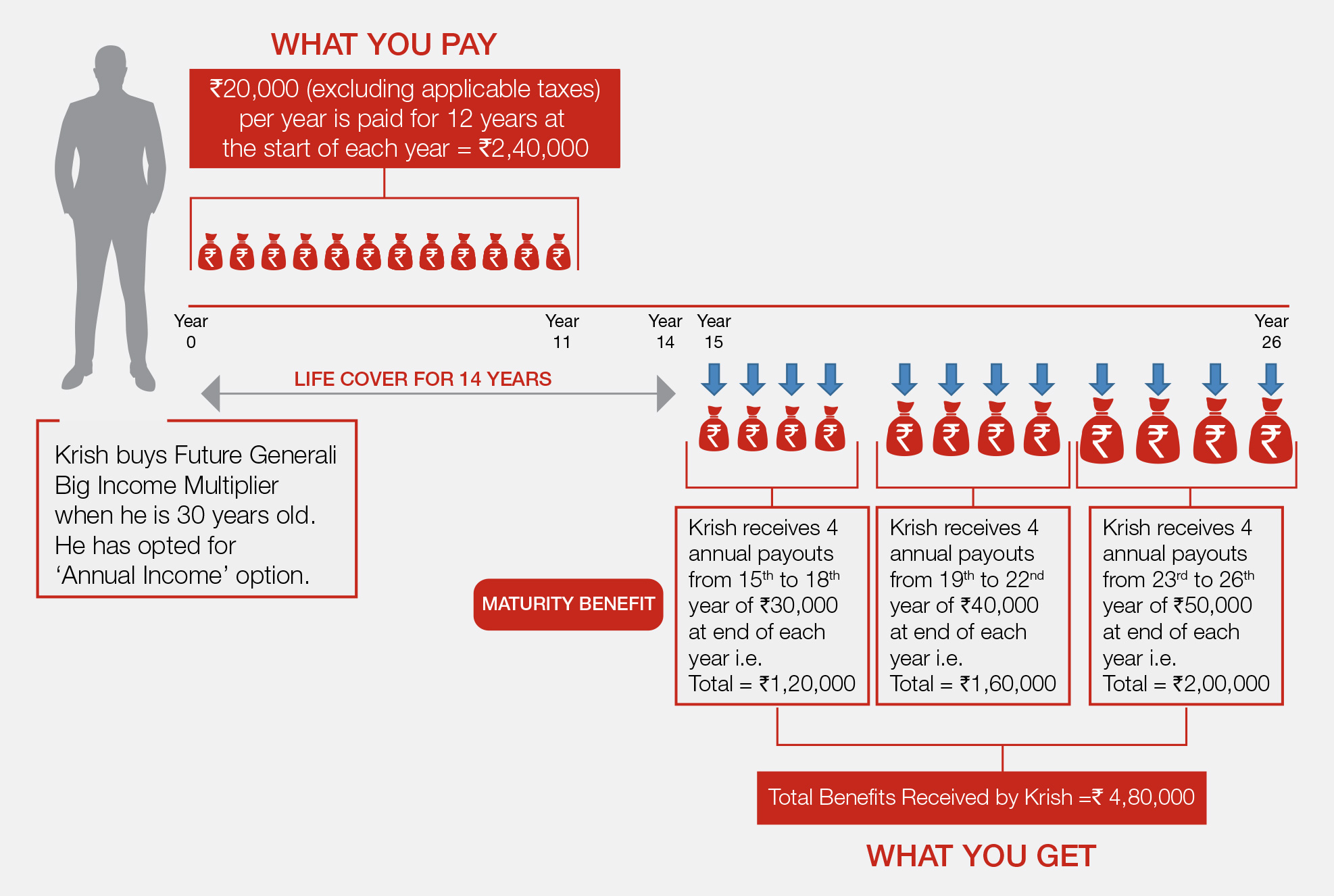

Let’s understand the life insurance plan with the help of an example:

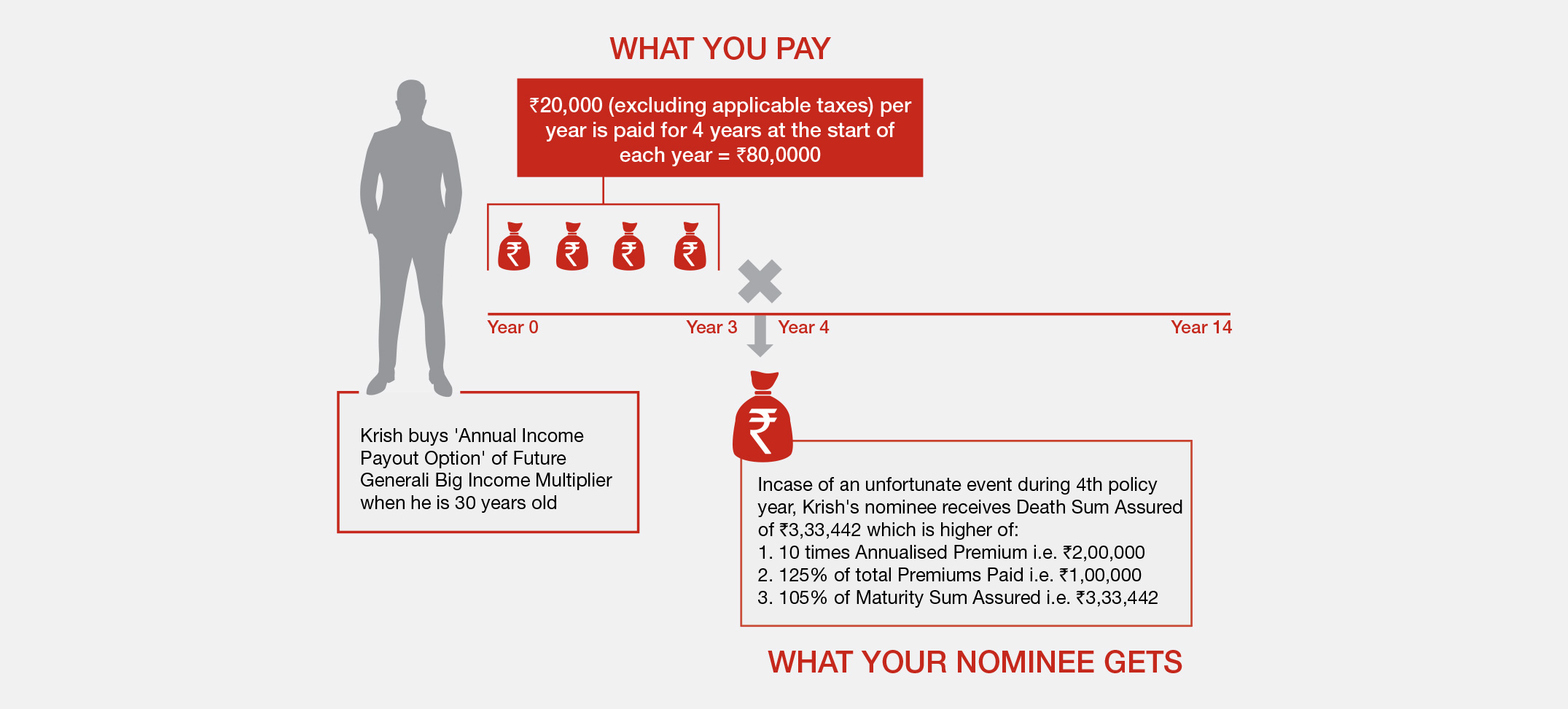

Krish is 30 years old and has purchased Future Generali Big Income Multiplier with an ‘Annual Income Payout Option’. He pays Rs. 20,000 as annual premium (excluding taxes, rider premiums, extra premiums and cess) for a premium payment term of 12 years. He will receive Rs. 4,80,000 over a period of 12 years after the end of policy term i.e. 14 years. Let us explain how?

Death Benefit

In case of your unfortunate demise during the Policy Term, a lump sum amount will be payable to your nominee as Death Sum Assured. In order to ensure that your family is always adequately protected, the Death Sum Assured shall be highest of the following:

| Age at Entry | Absolute amount payable on death as a percentage of Maturity Sum Assured | Age at Entry | Absolute amount payable on death as a percentage of Maturity Sum Assured |

|---|---|---|---|

| 4-10 yrs | 180% | 31-35 yrs | 85% |

| 11-17 yrs | 140% | 36-40 yrs | 70% |

| 18-25 yrs | 115% | 41-50 yrs | 65% |

| 26-30 yrs | 105% |

Note:

For example: Krish is 30 years old and has purchased Future Generali Big Income Multiplier with an ‘Annual Income Payout Option’ with an Annual Premium of Rs. 20,000 (excluding taxes, rider premiums, extra premium and cess). He pays the premium for 4 years and unfortunately passes away during the 4th policy year. In this case, Krish’s nominee will receive the following Death Benefit:

Grace Period: You get a grace period of 30 days if you have opted for annual premium payment or 15 days if you have opted for monthly premium payment from the premium due date to pay your missed premium.

During these days, you will continue to be covered and be entitled to receive all the benefits subject to deduction of due premium.

Free Look Period: In case you disagree with any of the terms and conditions of the policy, you can return the policy to the company within 15 days of its receipt for cancellation (30 days, if the policy is sold through the Distance Marketing Mode), stating your objections. Future Generali will refund the policy premium after the deduction of proportionate risk premium for the period of cover, stamp duty charges, cost of medical examination, if any.

Note: Distance Marketing means insurance solicitation by way of telephone calling/ short messaging service (SMS)/other electronic modes like e-mail, internet & interactive television (DTH)/direct mail/ newspaper & magazine inserts or any other means of communication other than in person.

If the Policy is opted through an Insurance Repository (IR), the computation of the said Free Look Period will be as stated below:-

Tax Benefits: Premium(s) paid are eligible for tax benefit as may be available under the provisions of Section(s) 80C and 10(10D) as applicable. For further details, consult your tax advisor. Tax benefits are subject to change from time to time.

Non-payment of premiums during the first 2 years

Non-payment of premiums post the first 2 years

Surrender Value The life insurance plan will acquire a surrender value after all the due premiums have been paid for the first 2 full policy years. The policy cannot be surrendered once the policy term is over. The surrender value payable is higher of the Guaranteed Surrender Value and the Special Surrender Value.

Guaranteed Surrender Value is as per the below table:

| Guaranteed Surrender Value | |

|---|---|

| Policy Year of Surrender | Guaranteed Surrender Value |

| 2 | 30% of premiums paid |

| 3 | 35% of premiums paid |

| 4 | 50% of premiums paid |

| 5 | 50% of premiums paid |

| 6 | 50% of premiums paid |

| 7 | 50% of premiums paid |

| 8 | 60% of premiums paid |

| 9 | 65% of premiums paid |

| 10 | 70% of premiums paid |

| 11 | 75% of premiums paid |

| 12 | 80% of premiums paid |

| 13 | 90% of premiums paid |

| 14 | 90% of premiums paid |

Premiums used for calculating guaranteed surrender value will be excluding taxes, rider premiums, extra premium and cess.

Special Surrender Value

Special Surrender Value = Special Surrender Value Factor x (Number of Instalment Premiums Paid / Total number of Instalment Premiums payable) * (Sum of total benefits payable during pay out period)

Special Surrender Value (SSV) factors will be based on the company’s expectation of future financial and demographic conditions and may be reviewed by the company from time to time with prior approval from IRDAI.

A policy terminates on surrender and no further benefits are payable under the policy.

Loan

You may avail of a loan once the policy has acquired a Surrender Value. The maximum amount of loan that can be availed is up to 85% of the Surrender Value. For more details, please refer to policy document.

The current interest rate for the financial year 2020-21 applicable on loans is 8% per annum compounded half yearly. Please contact our branch office or call us to know the current applicable interest rate.

Nomination and Assignment

Nomination, in accordance with Section 39 of the Insurance Act, 1938, as amended from time to time is permitted under this policy.

Assignment, in accordance with Section 38 of the Insurance Act, 1938, as amended from time to time is permitted under this policy.

Policy purchased under MWP( Married Women’s Property) Act cannot be assigned.

Riders

To enhance your financial protection and to secure yourself/your family against accidental disability or demise, we present to you Rider which you may choose as an additional protection. There is one rider option available under this plan: Future Generali Accidental Benefit Rider (UIN: 133B027V02)

Please refer to the respective rider brochure for more details.

Note: The premium pertaining to health related or critical illness riders shall not exceed 100% of premium under the basic product, the premiums under all other life insurance riders put together shall not exceed 30% of premiums under the basic product and any benefit arising under each of the above mentioned riders shall not exceed the sum assured under the basic product.

Suicide exclusion:

In case of death due to suicide within 12 months from the date of commencement of risk under the policy or from the date of revival of the policy, as applicable, the nominee or beneficiary of the policyholder shall be entitled to 80% of the total premiums paid till the date of death or the surrender value available as on the date of death whichever is higher, provided the policy is in force.

Prohibition on rebates:

Section 41 of the Insurance Act 1938 as amended from time to time states

1. No person shall allow or offer to allow, either directly or indirectly, as an inducement to any person to take or renew or continue an insurance in respect of any kind of risk relating to lives or property in India, any rebate of the whole or part of the commission payable or any rebate of the premium shown on the policy, nor shall any person taking out or renewing or continuing a policy accept any rebate, except such rebate as may be allowed in accordance with the published prospectuses or tables of the insurer.

2. Any person making default in complying with the provisions of this section shall be liable for a penalty which may extend to ten lakh rupees.

Section 45 of the Insurance Act 1938 as amended from time to time states

1. No Policy of Life Insurance shall be called in question on any ground whatsoever after the expiry of 3 years from the date of the policy i.e. from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later.

2. A policy of Life Insurance may be called in question at any time within 3 years from the date of issuance of the policy or the date of commencement of risk or the date of revival of the policy or the date of the rider to the policy, whichever is later, on the ground of fraud.

For further information, Section 45 of the Insurance laws (Amendment) Act, 2015 may be referred.

Future Generali India Life Insurance Company Limited is a joint venture between Future group, India’s leading retailer and Generali, an Italy based insurance major. The company was incorporated in 2006 and brings together the unique qualities of the founding companies - local experience and knowledge with global insurance expertise.

Future Generali India Life Insurance Company Limited offers an extensive range of life insurance products, and a network that ensures we are close to you wherever you go.

Future Generali Big Income Multiplier (UIN: 133N064V03)

POS Life variant of ‘Future Generali Big Income Multiplier’ is also available which can be applied without any medical examination up to limited Sum Assured, with waiting period for non-accidental death. Please click here for more details.

For detailed information on this product including risk factors, terms and conditions etc., please refer to the policy document and consult your advisor or visit our website before concluding a sale.

Riders are not mandatory and are available for an additional cost

Tax benefits are subject to change in law from time to time. You are advised to consult your tax consultant

The fine print in a policy can come in the way of making an informed purchase. We’ve simplified the fine print into big print.

Read the terms and conditions carefully. Ensure that your current health, occupation or lifestyle habits do not exclude you from getting the policy benefits.

Do's and don’ts to protect your life insurance policy from unauthorised elements posing as company representatives.

Find out how prepared you are to meet your financial goals, with our FutureReady calculator.

Buying a life insurance policy without asking your advisor the right questions is as good as crossing a road blindfolded.